There are two types of life insurance policies: term and permanent.

One of the most significant differences between the two is that term life insurance is a temporary product. It has an expiration date.

What happens when term life insurance expires? Your coverage ends, and you stop paying premiums.

In this guide, you’ll learn how long term life insurance lasts, what happens if you outlive your term life insurance, and if you can extend your coverage.

Table of Contents

- Do Life Insurance Policies Expire?

- How Long Does Term Life Insurance Last?

- What Happens at the End of Term Life Insurance?

- What to Do When Your Term Life Insurance Is Expiring

Do Life Insurance Policies Expire?

It depends on the type of policy you own:

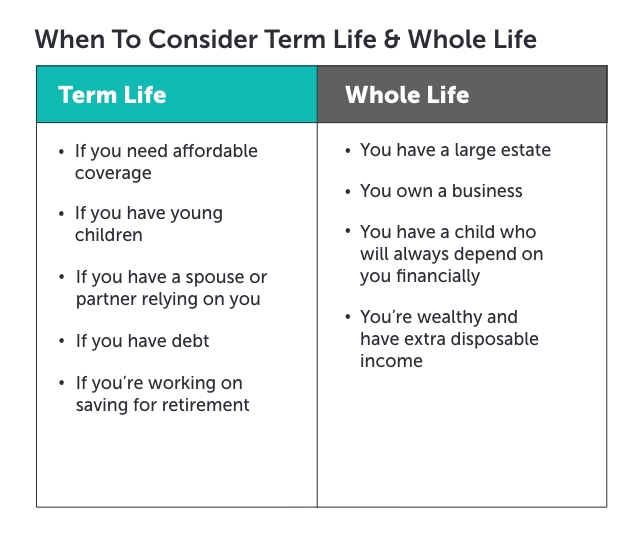

- Permanent life insurance products don’t expire. These policies, including whole and universal life, are designed to last your entire life.

- Term life insurance does expire. It’s designed to be temporary.

When life insurance coverage expires, you are no longer insured. If you die before the expiration date, your beneficiaries receive a death benefit check from the insurance company. If you die after the expiration date, your beneficiaries don’t receive a payout.

Do you need term life insurance or whole life insurance? Learn more about the differences between the two in our guide.

How Long Does Term Life Insurance Last?

Term life insurance offers fixed rates that last 10-40 years. So, if a 40-year-old buys a $500,000 20-year term policy for $30 per month, the cost remains $30 until it expires at age 60.

Ideally, you buy term life insurance to financially protect your loved ones during their most vulnerable years. The years when, if you were to die unexpectedly, they would struggle financially due to losing your income.

During these years, you may be:

- Raising children

- Saving for retirement

- Paying off a mortgage

- Running a business

If you were no longer around to provide for your loved ones, what would they do? This is why families should have term life insurance. It’s planning for the what-ifs.

Learn more: How Long Should My Term Life Insurance Last?

Not sure how much life insurance you need?

What Happens at the End of Term Life Insurance?

At the end of your policy’s term, you no longer have to pay any premiums, and your coverage ends. The insurance company will typically send you a notice informing you that your coverage has officially ended.

Can You Get Your Money Back?

If you outlive your term life insurance coverage, you only get a refund if you purchase return of premium life insurance. Because you get a refund if you don’t die, ROP term life insurance is more expensive than traditional level term life insurance.

For example, a healthy 40-year-old male can buy a traditional $500,000 term policy that lasts 20 years for $28.42 per month. The return of premium version would be $141.24 per month.

Most people choose the cheaper term policy since investing the difference over those 20 years often makes more financial sense.

What to Do When Your Term Life Insurance Is Expiring

If your term life insurance policy is ending and you want to continue to make sure your family is protected, you have some options:

- You can buy a new policy.

- You can convert the policy into a permanent one.

- You can renew your term coverage.

- You can go without life insurance.

Buying a New Policy

If your health hasn’t changed much, buying a new term policy will be the least expensive way to continue coverage. You don’t need to buy the same coverage amount or term length as your original policy.

For example, you purchased a 20-year term policy when your first child was born. You now have two children, one in college and one in high school. Perhaps you just want an additional 10-year term policy to ensure all your children are independent and no longer relying on you financially.

Converting Your Term Policy

Many term life insurance policies have a conversion rider automatically included. The rider would ensure you can convert your term policy into a permanent one regardless of your health status as long as you convert before the deadline.

The benefits of converting a term policy:

- You don’t have to go through underwriting or take a medical exam.

- You maintain the original health rating from the term policy.

- You can decide how much of the coverage to convert.

- You get life insurance coverage for your entire lifetime.

If you decide to convert, your premiums will increase drastically. You’ll no longer have a term policy. Instead, you’ll have a permanent policy, and permanent insurance is much more expensive.

If you’re interested in converting, check the conversion expiry date listed on your policy.

Renewing Your Term Coverage

Many insurance companies have renewability options on their term products. This means you can extend the coverage term year after year without having to re-qualify.

The catch is that renewable premiums are far higher than your initial fixed premium.

For example, you purchased a $500,000 20-year term life insurance policy when you were 30. Your annual cost is $244.

You’re now 50, and your policy expires this year. You can choose to renew the policy to extend the coverage another year. This means you’ll keep your $500,000 in coverage but no longer qualify for the $244 annual premiums. To renew the coverage, the annual premium is $2,989. Each year you renew, these premiums increase.

For people who are diagnosed with a severe medical condition, this option can be life-saving for your loved ones. Imagine your term insurance is about to expire, and you’re diagnosed with terminal cancer. You can opt to renew your coverage to ensure you don’t leave your family with a pile of medical bills.

The benefits of renewing a term policy:

- Allows you to reclaim your coverage at the end of your initial term.

- Allows you to keep your policy’s original face value amount (or death benefit).

- Permits you to renew your term life policy without starting the application process again.

- Exempts you from answering medical questions or undergoing a medical exam to prove insurability.

No Longer Have Life Insurance

If your expiration date is approaching, you can simply let the coverage run out. Depending on your situation and the stage of your life, you may not need life insurance anymore.

You likely do not need life insurance if:

- You have paid off your mortgage.

- You have no significant debt.

- You have no financially dependent children.

- Your spouse does not rely on your income.

- You’ve retired (or are retiring soon) and have sufficient savings.

If you currently own a term life insurance policy, check when the conversion period expires, when your term expires, and if it can be renewed. If you aren’t sure how to find this information on your policy, contact your life insurance agent or broker.

An annual policy review can help you ensure the end of your term policy doesn’t sneak up on you. Use our guide to understand when and why you should review your policy.

See what you’d pay for life insurance

Talk to a Quotacy Agent to Understand Your Policy Options

If the end of your term policy is approaching and you still want coverage, contact us here at Quotacy, and we can help you with the next step. Take a second to run a quote, too, so you know how much a new term policy may cost you.

You don’t have to spend time shopping from company to company. Our quoting tool lets you receive instant term life insurance quotes from multiple companies. When you’re ready, complete your application online, and your agent will shop your case to ensure you get the best price. You don’t have to keep your previous life insurance company. You always have options. Make the best of them.

Note: Life insurance quotes used in this article are accurate as of March 1, 2023. These are only estimates and your life insurance costs may be higher or lower.